What is a P-card?

A P-card (Purchasing Card), sometimes labeled a procurement card or university purchasing card, is a company-issued credit card that finance teams configure with vendor blocks, category limits, and budget caps.

Within a purchasing card program, employees complete a P-card application, and a P-card administrator activates the card under the broader P-card program policy. The card enables staff to purchase necessary supplies without raising purchase orders.

At the same time, finance teams track each transaction in real-time, eliminating manual paperwork and creating a procurement system that balances flexibility with control.

Modern organizations deploy P-cards in three formats:

- Physical cards enable in-person vendor transactions

- Virtual cards secure online purchases and subscriptions

- Single-use cards protect high-value, time-sensitive transactions

Each form manages specific business needs. Physical cards are helpful for office supply runs and managing local vendor relationships. Virtual cards excel at managing software subscriptions and online purchases. Single-use cards provide maximum security for large, one-time vendor payments.

How P-cards differ from traditional procurement

Traditional procurement requires multiple steps before employees can make purchases. Request forms move through approval chains. Purchase orders get created and sent to vendors. Invoices arrive weeks later for processing. This cycle consumes significant time and resources.

P-cards eliminate these inefficiencies through pre-configured spending controls. Administrators set rules once, and the system enforces them automatically. Employees make purchases within defined parameters. Transactions flow directly into accounting systems. The entire process happens without manual intervention.

P-cards vs. Corporate cards: A quick comparison

P-cards serve procurement purposes exclusively, whereas a corporate credit card, sometimes called a corporate card or travel card, is primarily designed for travel and entertainment expenses alongside vendor purchases.

Key operational differences include:

- Granular controls: P-cards restrict spending by vendor, category, and time

- Automated enforcement: Systems block non-compliant purchases instantly

- Procurement focus: Cards target vendor payments rather than employee expenses

- Real-time visibility: Administrators monitor transactions as they occur

- Purpose-built workflows: Approval processes align with procurement policies

Because the policies on a corporate credit card rely on after-the-fact expense reports, they typically lack the granular, real-time controls that define a P-card. For organizations that already issue a corporate credit card for travel and expense programs, adding a P-card complements rather than replaces that arrangement.

Corporate cards often rely on after-the-fact expense reports for control. P-cards prevent non-compliant spending before it happens. This proactive approach reduces policy violations and simplifies reconciliation.

How P-cards transform your procurement process

Launching or expanding a purchasing card program starts with selecting a platform, completing the P-card application, and appointing a P-card administrator who coordinates with procurement services. Many organizations pilot a small P-card program in one department before scaling company-wide.

As the program matures, finance teams expand limits, onboard more vendors, and benchmark results against industry leaders to ensure the purchasing card program continues to deliver savings and control. By treating the P-card as the organization's primary procurement card, teams gain rapid purchasing capability without sacrificing oversight.

Initial setup and configuration

Administrators issue P-cards through centralized platforms. Configuration happens before the first transaction:

- Card creation: Finance teams generate physical or virtual cards instantly

- Limit setting: Administrators define vendor lists, budgets, and categories

- Employee access: Authorized users receive cards with embedded restrictions

- Policy alignment: Controls match existing procurement guidelines

- System integration: Cards connect with accounting and ERP platforms

The setup process typically requires minimal IT involvement. Cloud-based platforms enable administrators to configure cards through intuitive interfaces. Most organizations complete the initial setup within days rather than weeks.

Transaction processing flow

At the point of sale, P-cards function like any payment card. The magic happens behind the scenes through automated policy enforcement:

- Purchase initiation: Employee presents P-card for payment

- Real-time validation: The System checks the transaction against configured rules

- Instant decision: Compliant purchases are approved automatically

- Data capture: Transaction details are recorded immediately

- Receipt management: Digital receipts are attached to transactions

- Accounting sync: Data flows into financial systems

Virtual P-cards function as periodic card numbers. Organizations configure them for specific vendors, periods, or purchase amounts. Some companies use a particular virtual period vendor relationship. Others create cards for specific projects or periods.

Post-transaction management

P-card systems continue working after the complete purchase. Automated processes handle traditionally manual tasks such as:

- Transaction categorization based on vendor and amount

- Expense coding using predefined rules

- Receipt matching through OCR technology

- Approval routing for exceptions

- Report generation for management review

These automated workflows free finance teams from routine tasks. Staff members focus on analysis and strategy rather than data entry and filing.

8 strategic benefits that drive P-card adoption

Organizations implement P-cards to achieve specific business outcomes. These benefits demonstrate why finance leaders prioritize P-card programs.

1. Eliminate administrative burden

P-cards remove manual processes that delay business operations. Finance teams save hours daily through automation. The cumulative impact transforms how organizations operate.

Traditional procurement creates administrative overhead at every step. Employees fill out requisition forms. Managers review and approve requests. Purchasing departments create formal purchase orders. Vendors process orders and ship goods. Accounting departments handle invoices weeks later. Each step requires human intervention and creates potential delays.

P-cards compress this multi-step process into a single transaction. Employees purchase what they are allowed to within predefined limits. The transaction records automatically. Receipts are captured digitally. Accounting entries are generated without manual input.

Organizations achieve these operational improvements:

- Purchase orders disappear from routine transactions

- Approval chains shrink from weeks to seconds

- Expense categorization happens automatically

- Receipt capture occurs at the point of sale

- Invoice processing becomes unnecessary

- Check runs have reduced significantly

2. Gain complete financial control

Real-time controls prevent overspending before it happens. P-cards enforce budgets proactively rather than discovering violations later. This fundamental shift changes how organizations manage spending.

Traditional controls rely on review and approval processes. Someone requests a purchase. Multiple people review the request. Eventually, someone approves or denies it. This process takes time and still allows policy violations to occur. By the time finance discovers an issue, the money is already spent.

P-cards embed controls directly into the payment mechanism. Configuration determines what employees can buy, where they can buy it, and how much they can spend. These rules apply instantly at the point of sale. Non-compliant purchases simply don't process.

Financial oversight features include:

- Merchant category restrictions block unauthorized purchases

- Transaction limits prevent excessive spending

- Budget caps align with fiscal periods

- Geographic controls enhance security

- Scheduled activation prevents off-hours use

- Velocity controls limit transaction frequency

Advanced systems provide even more sophisticated controls. Some organizations restrict cards to specific SKUs or product categories. Others implement dynamic limits that adjust based on budget availability. The flexibility enables precise control without creating an administrative burden.

3. Strengthen vendor partnerships

Traditional procurement creates cash flow challenges for vendors. They fulfill orders, submit invoices, and wait for payment. The waiting period might extend 30, 60, or even 90 days. Small vendors particularly struggle with these delays. Some increase prices to compensate for slow payment. Others simply refuse to work with slow-paying organizations.

P-cards improve vendor interactions by:

- Guaranteeing payment upon delivery

- Reducing invoice processing costs

- Eliminating payment delays

- Simplifying reconciliation processes

- Removing collection activities

- Improving vendor satisfaction scores

Many vendors prefer customers who use P-cards. Some offer discounts for P-card payments. Others provide preferential service to P-card customers. The mutual benefits create win-win relationships.

4. Enhance security and compliance

P-cards provide superior protection compared to traditional payment methods. Built-in controls prevent fraud before it occurs. Multiple security layers protect organizations from various threats.

Security advantages include:

- Elimination of check fraud risks

- Complete transaction audit trails

- Real-time monitoring capabilities

- Multi-factor authentication

- Automated policy enforcement

- Instant card deactivation options

- Limited employee liability

- Fraud protection guarantees

Compliance features address regulatory and internal policy requirements. P-card systems maintain detailed records for audit purposes. They enforce spending policies automatically. They generate reports for tax and regulatory filings. These capabilities reduce compliance costs while improving accuracy.

5. Generate revenue through rebates

Organizations earn cash back on every P-card transaction. These rebates provide direct bottom-line impact. Innovative organizations treat rebate revenue as a strategic opportunity.

Revenue generation occurs through:

- Volume-based rebate percentages

- Consolidated spending power

- Strategic vendor selection

- Optimized purchase timing

- Negotiated rate improvements

Maximizing rebate revenue requires strategic thinking. Organizations analyze spending patterns to identify rebate opportunities. They consolidate purchases to achieve volume thresholds. They negotiate with card providers for better rates. They shift spending from other payment methods to P-cards.

6. Reduce operational costs

P-cards eliminate expensive manual processes, allowing organizations to divert resources toward strategic initiatives.

P-cards reduce or eliminate many cost categories:

- Decreased accounts payable staffing needs

- Eliminated paper processing expenses

- Reduced reconciliation time

- Lower fraud investigation costs

- Decreased storage requirements

- Reduced mailing and printing costs

- Minimized dispute resolution expenses

Technology costs also decrease with P-card adoption. Organizations need fewer approval workflow systems. They process fewer invoices through accounts payable systems. They generate fewer checks through payment systems. The cumulative technology savings can be substantial.

7. Automate procurement workflows

Technology transforms procurement from manual tasks to automated workflows. Finance teams focus on analysis rather than data entry. This shift represents one of P-cards' most valuable contributions.

Manual procurement workflows consume enormous time. Each step requires human attention. Errors create rework. Delays compound throughout the process. Finance teams spend most of their time on routine tasks rather than strategic activities.

Automation capabilities deliver:

- Real-time transaction alerts

- Automatic receipt matching

- Instant expense coding

- Seamless ERP integration

- Compliance report generation

- Budget tracking updates

- Vendor spend analysis

- Exception identification

Modern P-card platforms use artificial intelligence to enhance automation. Machine learning algorithms improve categorization accuracy. Predictive analytics identifies potential issues before they occur. Natural language processing extracts data from receipts automatically.

8. Accelerate business operations

P-cards provide speed without sacrificing control. Pre-configured limits enable instant decisions. Employees purchase what they need immediately. Operations continue without procurement delays.

Acceleration benefits include:

- Instant vendor payments

- Eliminated reimbursement delays

- Streamlined approval processes

- Reduced administrative bottlenecks

- Faster project completion

- Improved employee satisfaction

- Enhanced operational agility

The speed advantage becomes particularly important for time-sensitive purchases. Emergency repairs happen immediately. Project supplies arrive when needed. Sales opportunities don't slip away due to procurement delays.

Selecting your P-card management approach

Organizations choose between three management methods based on transaction volume and automation needs. Each approach offers different benefits and challenges.

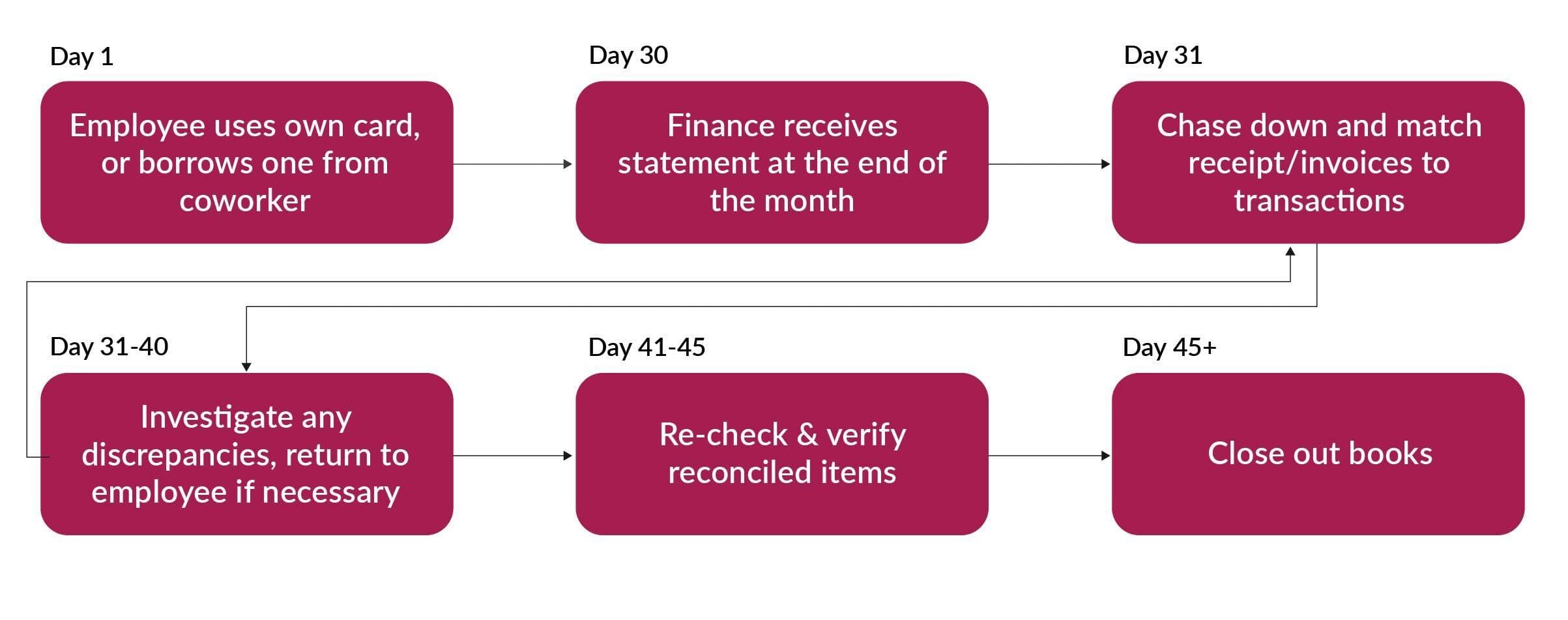

Manual management (spreadsheets/paper)

Small organizations with minimal transactions may use manual processes. This approach requires a significant time investment but minimal technology costs.

The manual process typically follows these steps:

- Monthly transaction downloads from the card provider

- Manual receipt collection from employees

- Spreadsheet-based transaction matching

- Manual coding and categorization

- Paper-based approval workflows

- Manual entry into accounting systems

This approach requires approximately 45 days for complete reconciliation. The timeline assumes no complications or missing receipts. Most organizations experience longer cycles due to inevitable delays.

Best for

Organizations with fewer than 50 monthly transactions and limited technology budgets

Advantages

Low technology costs, complete control over processes, no training requirements

Disadvantages

High labor costs, increased error rates, slow processing times, limited visibility

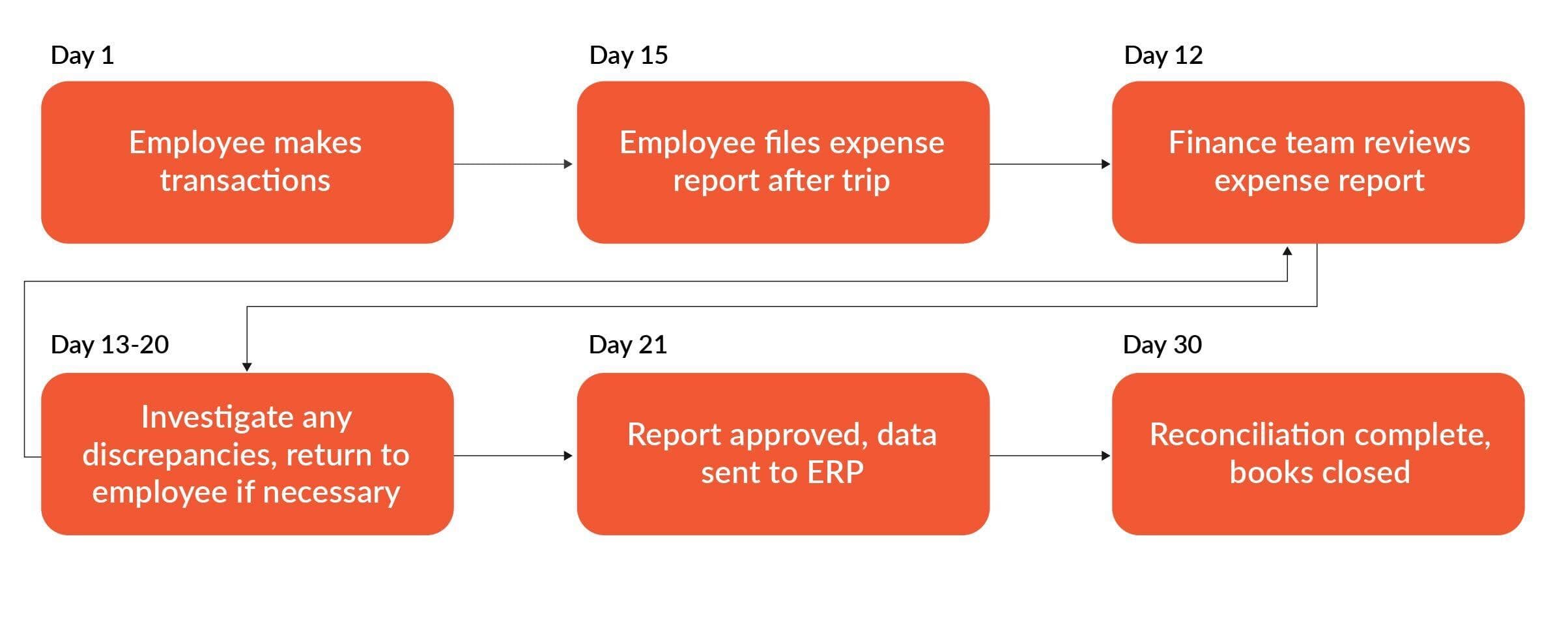

Traditional expense reports

Mid-size companies often process P-card transactions through expense report systems. This method provides basic automation while leveraging existing infrastructure.

The expense report process improves on manual methods:

- Automated transaction imports

- Digital receipt attachment

- Basic approval workflows

- Bulk transaction processing

- Integration with accounting systems

- Standard reporting capabilities

Processing typically requires 30 days from transaction to reconciliation. The timeline depends on employee submission habits and month-end close schedules.

Best for

Companies with established expense report processes and moderate transaction volumes

Advantages

Leverages existing systems, provides basic automation, maintains familiar processes

Disadvantages

Treats procurement like T&E expenses, delays processing, limits real-time visibility

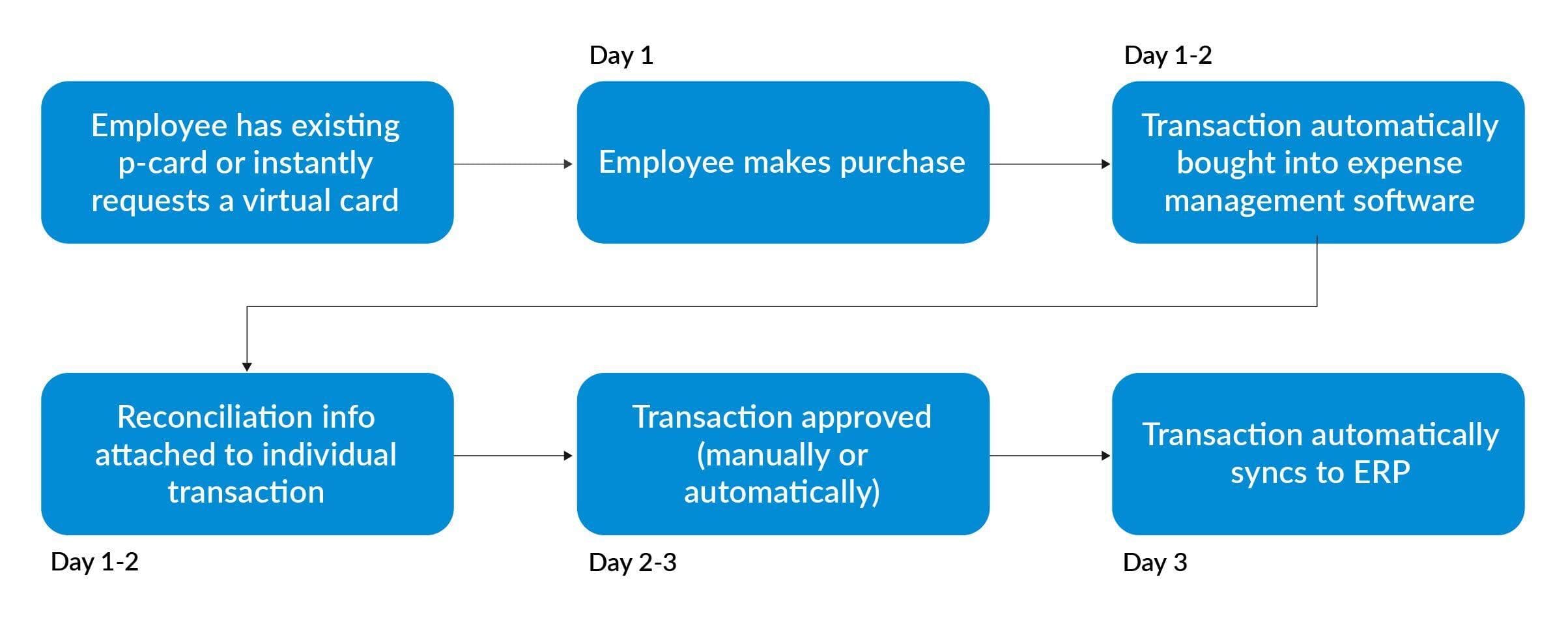

Dedicated expense management software

Modern platforms process P-card transactions individually in real-time. Advanced systems deliver comprehensive automation and control capabilities.

Dedicated software transforms P-card management:

- Point-of-sale data capture

- Intelligent categorization

- Policy-based auto-approval

- Instant ERP synchronization

- Real-time spend visibility

- Advanced analytics capabilities

Transactions are entirely processed within hours rather than weeks. Most transactions require no human intervention beyond the initial purchase.

Best for

Organizations prioritizing automation and control, regardless of size

Advantages

Maximum automation, real-time processing, comprehensive controls, strategic insights

Disadvantages

Higher initial investment, change management requirements, integration complexity

Transform your P-card management solution with Emburse

P-cards revolutionize how organizations manage vendor spending. Finance leaders who implement comprehensive P-card programs eliminate manual workflows while gaining unprecedented spending control. Modern expense management platforms amplify these benefits through automation and real-time visibility.

Ready to modernize your procurement process? Discover how automated P-card management eliminates manual workflows while providing complete spending control.

Request a personalized demonstration to see your potential time and cost savings with a customized implementation plan.

FAQs about P-cards

How do P-card payments work?

P-card payments run on standard card networks while your company settles on a statement.Here is the flow in plain language:

- The network authorizes the purchase against your rules for amount, timing, and merchant category.

- The merchant is funded by its acquirer, and your company pays the issuer on a consolidated statement.

- Level 2 and Level 3 data can provide richer line items, and disputes follow standard card rules.

How quickly can organizations implement P-card programs?

Most teams can stand up a basic P-card program in about 30 days.Use these timelines as a realistic planning baseline:

- Typically, the launch process takes about 30 days for provider selection, policy setup, training, and integrations.

- Complex environments often require 60 to 90 days for full deployment.

- Phased rollouts usually work better than big-bang launches.

What transaction volumes justify P-card adoption?

Transaction volume helps, but objectives and controls matter more.Use these rules of thumb:

- Clear ROI once you process more than 100 vendor transactions per month.

- Smaller companies still gain through lower processing costs and stronger controls.

- Prioritize the outcomes you want, such as control, speed, and visibility, over raw volume.

Can P-cards integrate with existing accounting systems?

Yes, modern platforms integrate with major ERPs without a heavy IT lift.Expect the following integration patterns:

- Native or certified connectors for SAP, Oracle, NetSuite, QuickBooks, and similar systems.

- Real-time or scheduled sync that reduces manual entry and reconciliation.

- Prebuilt connectors and open APIs that are configured during implementation.

How do virtual P-cards enhance security?

Virtual cards reduce fraud exposure by isolating risk to a single vendor or transaction.Security benefits include:

- Unique numbers per transaction or vendor, including single-use options.

- If compromised, exposure is limited to that number rather than the entire account.

- Administrators can issue, adjust, and revoke virtual cards instantly.

How do organizations maximize P-card rebate revenue?

Rebates grow with compliant volume and disciplined vendor strategy.Focus on these levers:

- Shift eligible spend from checks and ACH to P-cards to reach higher rebate tiers.

- Negotiate rates using credible volume forecasts and category plans.

- Analyze spend to target rebate-friendly categories and align vendor selection and payment timing.

- Expect rebate growth over time as adoption and managed categories expand.

What is spend management?

Spend management is the framework and tools that govern how money leaves your company. At a minimum, an effective program includes:

- Policies and processes to plan, control, and analyze spend across cards, invoices, and travel and expense.

- Software that supports budgets, approvals, vendor controls, real-time monitoring, and analytics.

- P-cards are one lever within a broader program rather than a standalone solution.