For years, expense fraud followed a familiar pattern.

An employee rounded up a meal cost. A duplicate receipt slipped through. A personal purchase found its way into an expense report.

While frustrating, these issues were generally limited by human effort. Creating convincing documentation required time, skill, and the willingness to take a risk.

AI has changed the equation.

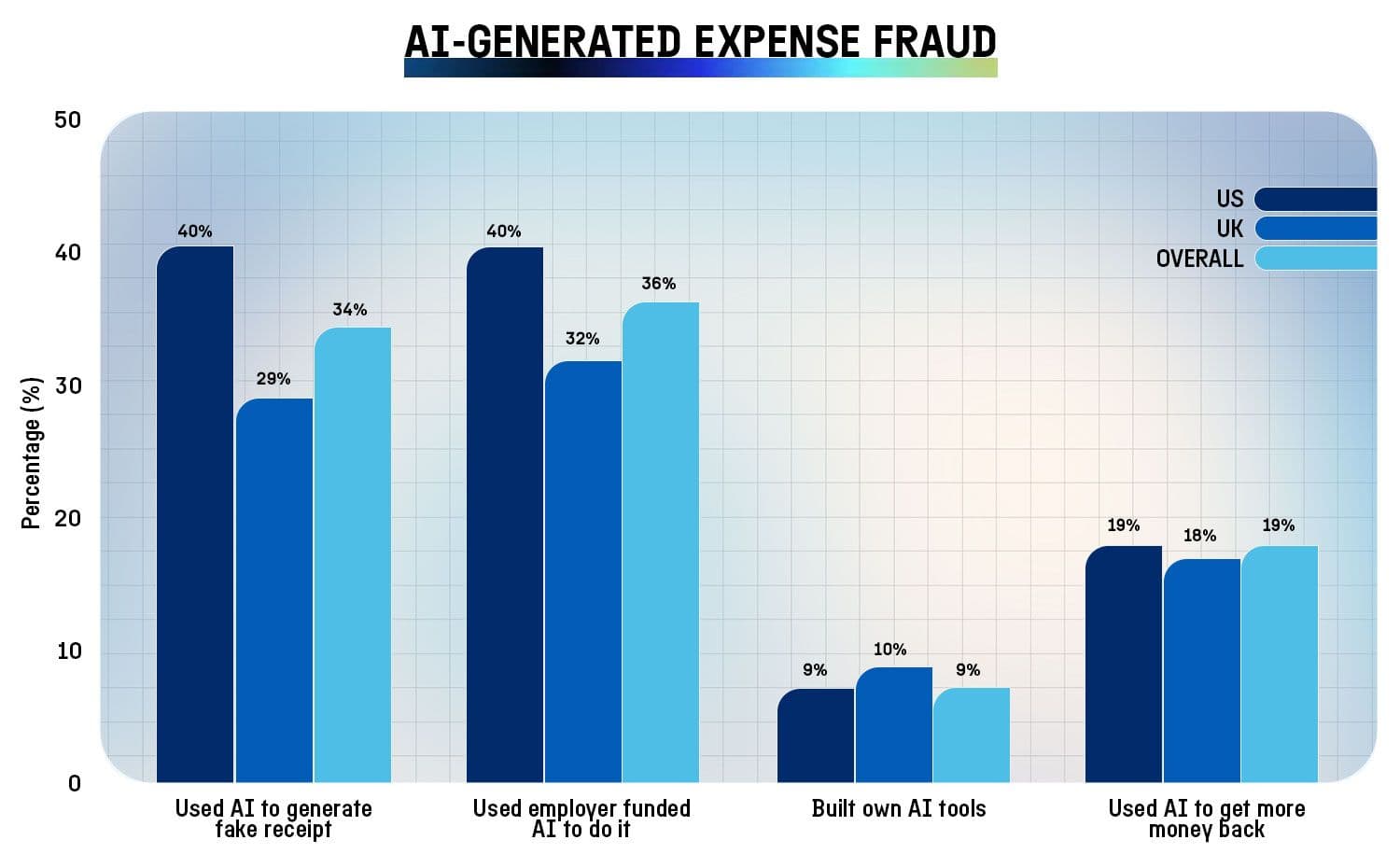

AI-generated receipts are making expense fraud faster, easier, and harder to detect with traditional controls. New Emburse research surveying 2,000 business professionals across the U.S. and UK found that 34% of respondents admit they have used AI to generate a fake receipt for a business expense. U.S. respondents reported the behavior at a higher rate, with 40% saying they have done so, compared with 29% of UK respondents.

Even more concerning, 36% say they used AI tools funded by their employer to generate those receipts.

The headline is striking. But the real story isn’t simply about fake receipts.

It’s about how financial pressure, changing employee expectations, and rapidly evolving technology are reshaping the relationship between employees, employers, and expense compliance.

This is why finance leaders need to rethink trust in the age of AI.

How AI-generated receipts are changing expense fraud

Historically, expense fraud was constrained by opportunity.

An employee might submit a questionable claim here or there, but creating entirely fabricated documentation that could withstand scrutiny required a level of sophistication most people didn't possess.

Today, generative AI can produce realistic-looking receipts, invoices, and supporting documents in seconds.

The barrier to entry has effectively disappeared.

What's particularly notable about the survey findings is why employees are using AI to create fraudulent receipts.

The most common reason isn't replacing a lost receipt or recreating legitimate documentation.

It's to receive more money than they actually spent.

Nineteen percent of respondents overall admitted using AI-generated receipts to obtain a larger reimbursement than the original purchase amount. The figure was nearly identical across markets, with 19% in the U.S. and 18% in the UK.

This represents a fundamental shift in modern expense risk.

The challenge is no longer simply identifying accidental mistakes or policy misunderstandings.

Finance teams must now contend with technology capable of generating highly convincing fraudulent documentation at scale.

Why reimbursement delays can increase expense compliance risk

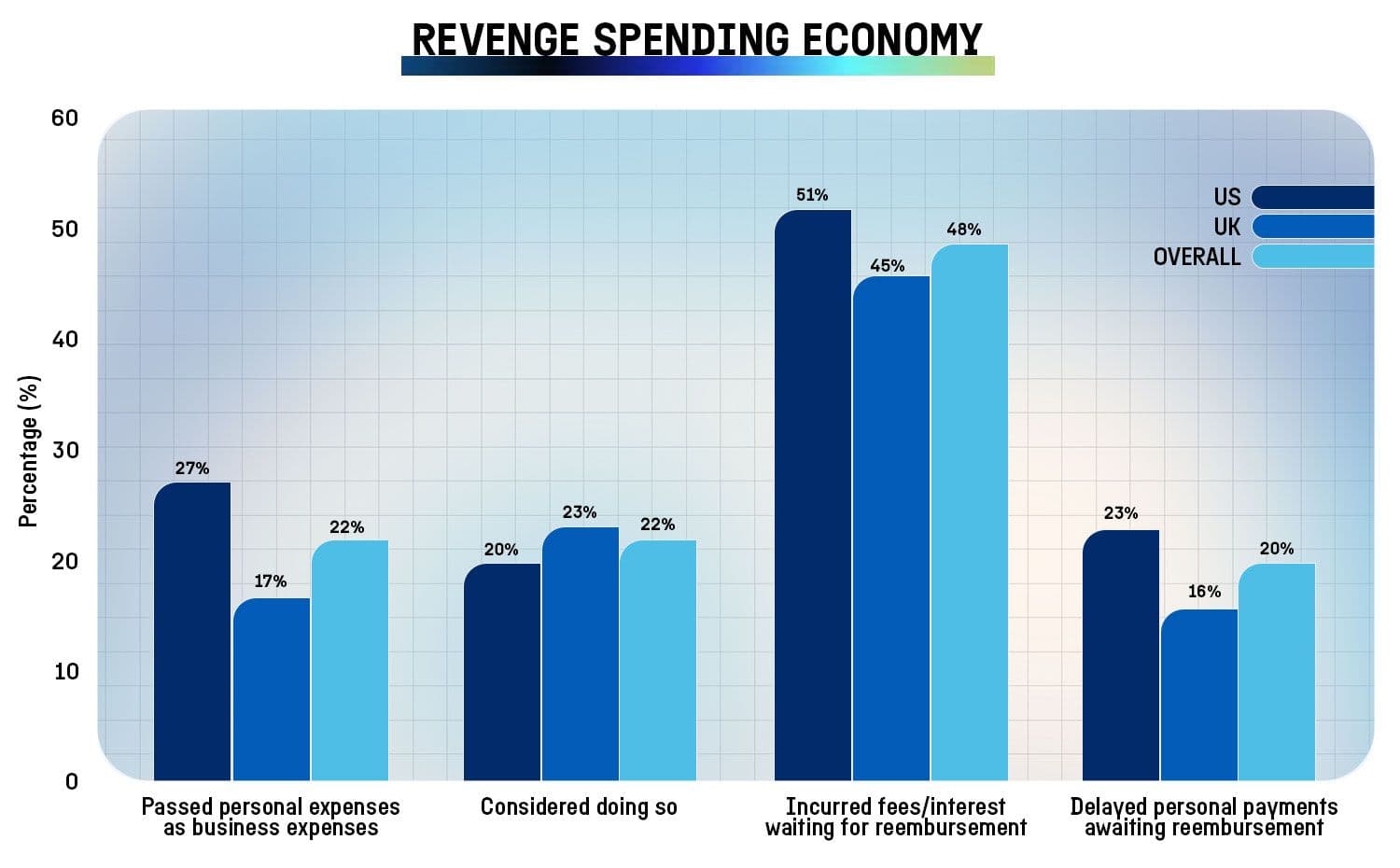

One emerging behavior in the data is what Emburse calls revenge spending: employees submitting personal purchases as business expenses because financial pressure or reimbursement frustration has changed how they view workplace spend.

When asked whether they had ever made a personal purchase and submitted it as a business expense because of their financial circumstances, 22% of respondents overall said yes. The data suggests that reimbursement friction is not just an employee experience issue. It can become a compliance risk.

U.S. respondents reported this behavior at a higher rate, with 27% admitting to having done so. Just 17% of UK respondents indulged in this behavior.

Another 22% said they have considered doing so but ultimately chose not to.

This trend appears to be growing.

In the U.S., the percentage of employees who admitted to revenge spending increased compared to Emburse's 2024 research. Particularly notable was the increase among employees aged 55 and older, rising from 4% in 2024 to 11% in 2026.

While revenge spending is often viewed solely as misconduct, the data suggests a more complicated reality.

Many employees appear to be responding to financial pressures created by the reimbursement process itself.

Among respondents who admitted to passing personal purchases off as business expenses:

- 76% of U.S. respondents and 74% of UK respondents said they were somewhat or very concerned about their personal finances.

- 51% of U.S. respondents and 45% of UK respondents incurred overdraft fees, late-payment charges, excess fees, or credit card interest while waiting for reimbursement.

- 29% of U.S. respondents and 21% of UK respondents incurred interest on personal credit cards because reimbursement took too long.

- 23% of U.S. respondents and 16% of UK respondents delayed personal purchases or bill payments while waiting to be reimbursed.

None of this excuses fraudulent behavior.

But it does highlight an important reality: compliance challenges often begin long before an expense report reaches the finance team.

When employees repeatedly front business costs, absorb financial consequences, and wait extended periods for reimbursement, frustration can become a risk factor.

In other words, fraud prevention isn't only about detection.

It's also about reducing the conditions that make non-compliant behavior more likely in the first place.

Why employees are shifting toward corporate cards

Perhaps the clearest signal from this year's research is employees' growing preference for corporate cards.

For years, many employees preferred using personal cards to earn rewards points, travel benefits, or cash back.

That trend appears to be reversing.

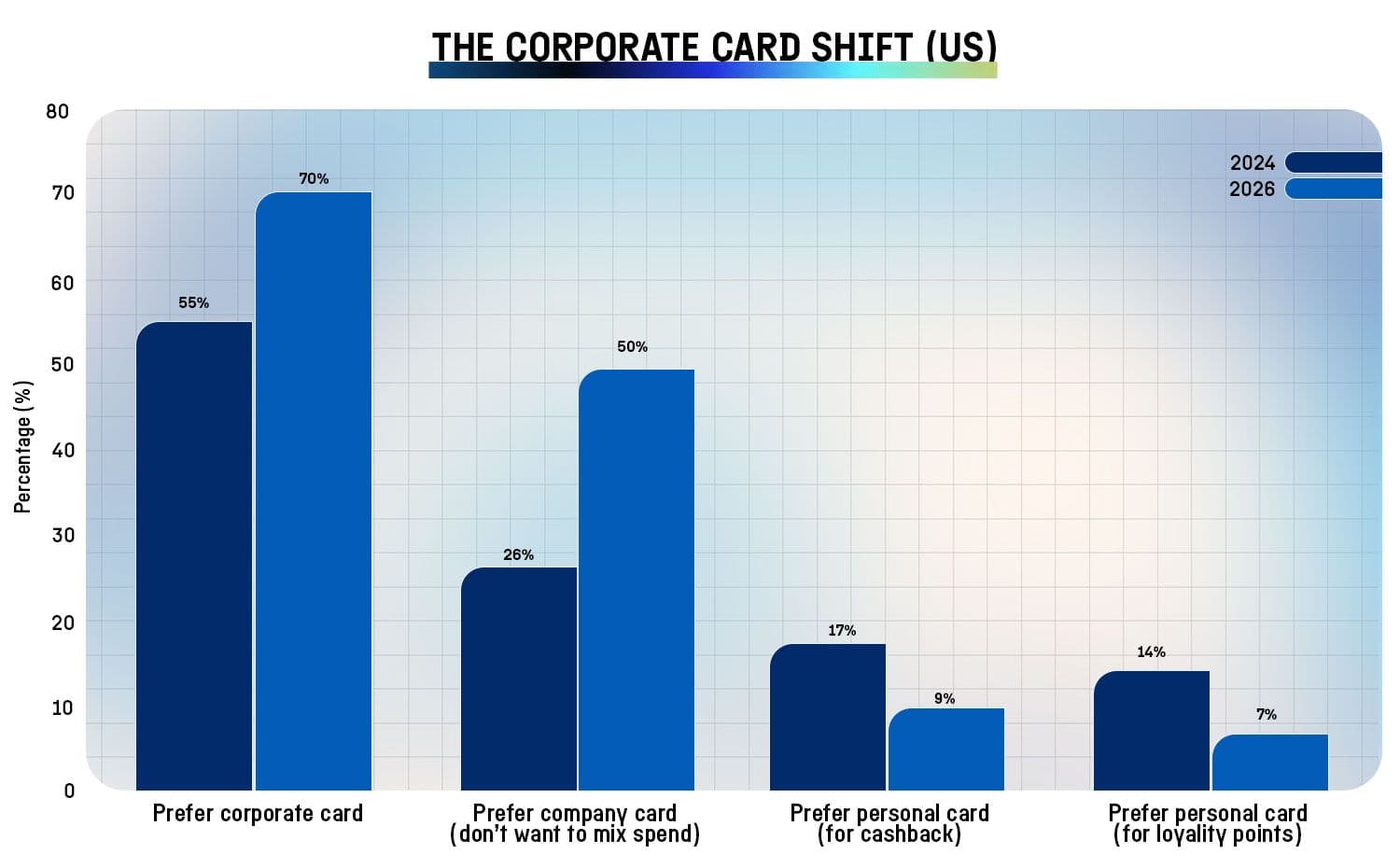

When asked why they would prefer a company card for work-related purchases, the most common response was simple:

"I don't want to mix personal and business spending."

In the U.S., agreement with that statement nearly doubled, rising from 26% in 2024 to 50% in 2026.

The figure reached 52% in the UK and 51% overall.

Frustration with reimbursement timelines is also becoming more apparent.

The percentage of U.S. employees who said they prefer company cards because expense processing takes too long increased from 10% in 2024 to 16% in 2026. The figure was even higher in the UK at 21%.

At the same time, motivations for using personal cards are declining.

Among U.S. respondents:

- Preference for personal cards to earn cash back declined from 17% to 9%.

- Preference for earning airline and hotel loyalty points declined from 14% to 7%.

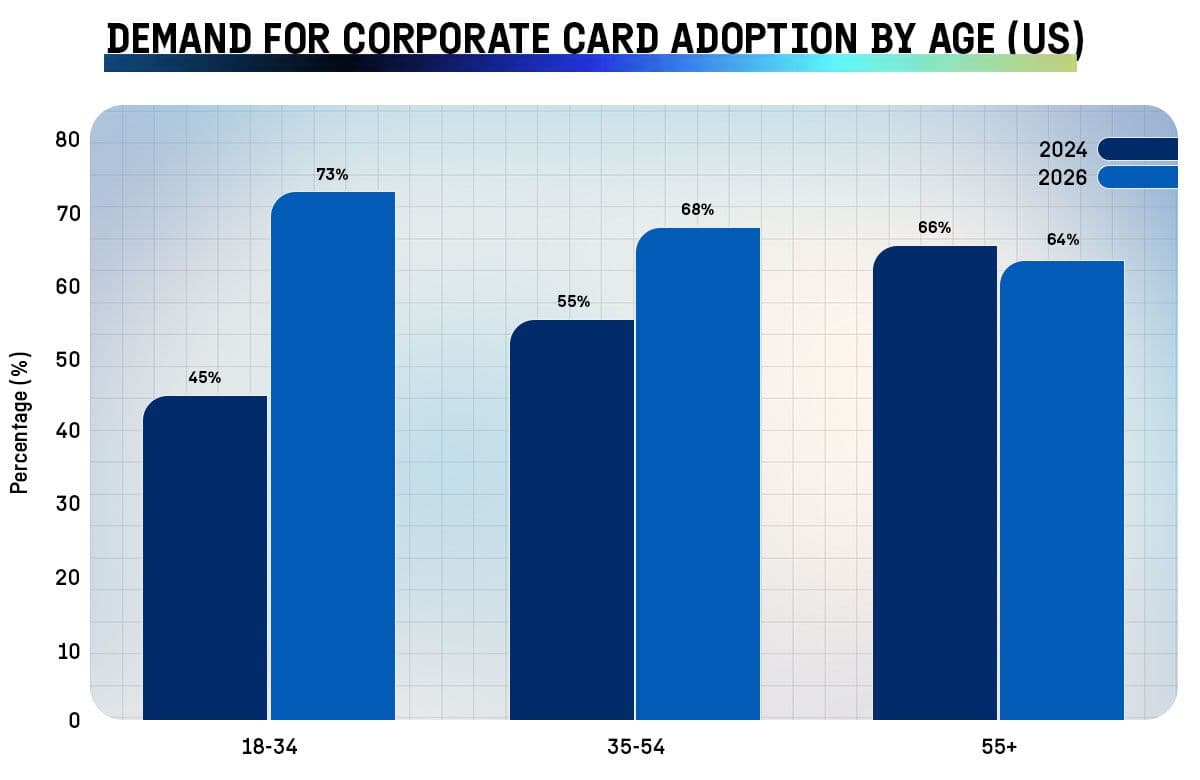

Younger employees appear to be driving much of this shift, suggesting that corporate card adoption is becoming tied to changing expectations around financial burden and workplace experience.

Among U.S. respondents:

- Ages 18-34 increased their preference for company cards from 45% to 73%.

- Ages 35-54 increased from 55% to 68%.

- Ages 55+ remained largely unchanged.

Employees are sending a clear message. The perceived benefits of personal rewards are increasingly outweighed by the financial and administrative burden of fronting business expenses.

Corporate card programs, including Emburse Cards, can reduce the need for employees to front business expenses while giving finance teams more visibility and control over spend.

How employer-funded AI tools are creating new governance risks

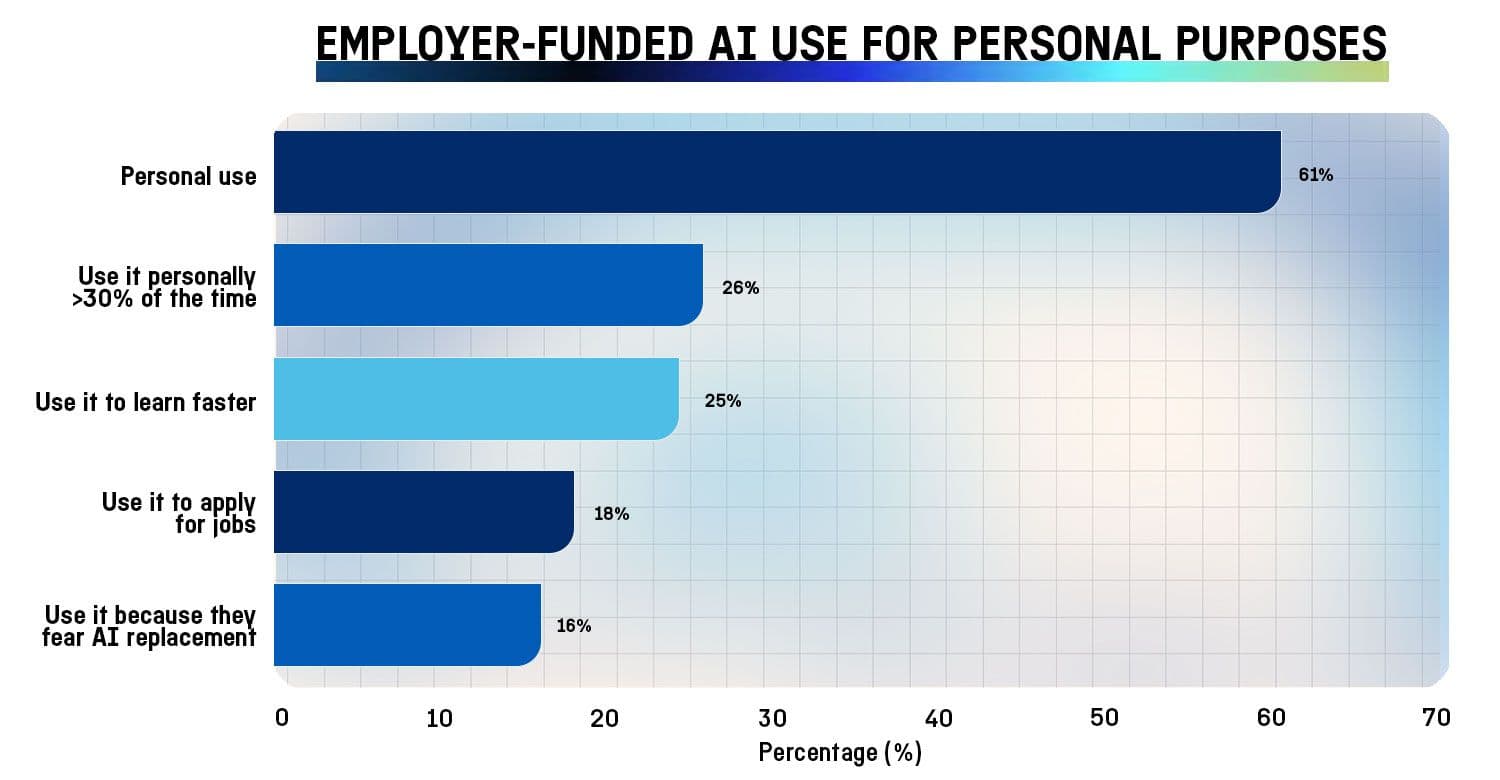

The survey uncovered another emerging challenge.

Employees are increasingly using AI tools funded by their employers for personal purposes.

Overall, 61% of respondents reported using employer-funded AI tools outside of work-related activities. The figure reached 63% in the U.S. and 59% in the UK. The personal use of employer-funded AI tools points to a broader governance issue that extends beyond expense reports.

More notably, 26% of respondents said personal activities account for more than 30% of their AI usage.

Some are using AI to plan vacations, manage personal projects, or learn new skills.

Others are using employer-funded AI for activities that create governance concerns.

Eighteen percent of respondents reported using employer-funded AI tools to apply for other jobs.

The motivations are revealing.

The most common reason employees cited was practical: they believe AI helps them become more efficient and effective in their personal lives, ultimately making them better employees.

Other motivations included:

- Learning AI skills faster (25% overall)

- Taking advantage of expensive tools they couldn't justify purchasing personally (13% overall)

- Not realizing their employer prohibited personal use (23% overall)

- Concerns that AI may eventually replace their jobs (16% overall)

- Access to large, underutilized AI budgets or token allocations (14% overall)

Taken together, these findings suggest organizations are facing a broader governance challenge.

The question is no longer simply:

"Who submitted this expense?"

Increasingly, finance and business leaders are asking:

- Which AI tools are employees using?

- What are they being used for?

- How much spend is associated with those tools?

- Are company resources being used in ways that align with organizational policies?

These are visibility questions as much as compliance questions.

As AI becomes embedded in everyday workflows, finance and business leaders need clear visibility into how tools are used, what they cost, and how purpose-built systems like Emburse AI can support more accurate, controlled spend decisions.

Why traditional expense controls are no longer enough for AI-generated fraud

Many expense processes were designed for a world where fraud was manual, documentation was static, and policy enforcement happened after money had already been spent.

That world is disappearing.

As AI becomes more accessible, organizations need controls that are equally intelligent.

They need systems capable of:

- Detecting fabricated receipts and altered documentation

- Identifying unusual reimbursement patterns

- Monitoring spend anomalies across departments and vendors

- Providing real-time visibility into AI subscriptions and software purchases

- Guiding employees toward compliant behavior before reimbursement occurs

Perhaps most importantly, organizations need greater visibility into spend before risk materializes. The companies that succeed won't be the ones that assume every employee is acting in bad faith – they'll be the ones that recognize compliance, employee experience, financial well-being, and governance are increasingly interconnected.

AI-powered expense compliance solutions like Emburse Assurance can help finance teams review receipt details in context, guide employees before submission, and surface higher-risk activity after submission.

What finance leaders should do now

AI-generated receipts are not just a fraud problem. They are a control, visibility, and employee experience problem. Finance leaders should focus on five priorities:

1. Move controls earlier in the expense process

Policy guidance should happen before submission, not only after an expense reaches finance. Real-time prompts, pre-submission checks, and embedded policy reminders can help employees correct issues before they create rework or risk.

2. Reduce reimbursement friction

Delayed reimbursements can create financial stress for employees and frustration with the expense process. Faster, cleaner workflows reduce the burden on employees and lower the conditions that can make non-compliant behavior more likely.

3. Expand corporate card use where appropriate

Corporate cards can reduce the need for employees to front business expenses while giving finance teams better visibility and control. As employees become less interested in mixing personal and business spend, corporate cards can support both employee experience and stronger governance.

4. Use AI to evaluate context, not just extract text

Receipt review needs to account for merchant details, line items, categories, timing, duplicate patterns, and behavioral anomalies. In an AI-generated fraud environment, simply confirming that a receipt exists is no longer enough.

5. Govern employer-funded AI tools like a spend category

AI subscriptions and usage should be visible, policy-aligned, and connected to broader spend management controls. Finance and business leaders need to understand which tools are being used, what they cost, and whether they align with company policy.

In the age of AI, expense management software needs to do more than track what happened. It needs to help finance teams guide what happens next.

The goal is not to treat every employee as a risk. It is to build a system where trust is easier to maintain. In the age of AI, finance teams need controls that work before, during, and after spend happens. With Emburse Expense Intelligence, organizations can move from after-the-fact reconciliation to real-time spend control, helping teams reduce risk, guide compliant behavior, and protect the business without slowing people down.

Methodology

Emburse commissioned Atomik Research to conduct an online survey of 1,000 professionally employed adults 18+ throughout the United States and 1,000 professionally employed adults 18+ throughout the United Kingdom. The margin of error is +/-3 percent with a confidence level of 95 percent. Fieldwork took place between May 5 to 8, 2026.

Atomik Research is an independent creative market research agency with its global headquarters in Bentonville, Arkansas.

The 2024 survey results are based on a study from YouGov Plc. The total sample size was 1,021 adults aged 18-64, employed full-time. Fieldwork was undertaken between 5th - 11th of January 2024. The survey was carried out online.

Frequently asked questions about AI-generated receipts and expense fraud

What are AI-generated receipts? AI-generated receipts are fabricated or altered receipt images created with generative AI tools. They can appear realistic enough to pass basic visual checks, especially when expense processes rely on manual review or simple receipt attachment rules.

Why are AI-generated receipts a problem for finance teams? AI-generated receipts lower the effort required to create convincing false documentation. That means finance teams must evaluate not only whether a receipt exists, but whether the receipt, amount, merchant, category, timing, and employee behavior make sense together.

How common is AI-generated receipt fraud? In Emburse’s 2026 survey of 2,000 U.S. and UK business professionals, 34% of respondents said they have used AI to generate a fake receipt for a business expense.

How can companies reduce AI-generated receipt fraud? Companies can reduce risk by combining corporate cards, faster reimbursement processes, real-time policy guidance, anomaly detection, and AI-powered receipt review. The goal is to prevent errors early, surface suspicious activity faster, and reduce manual review burden for finance teams.

What is the difference between traditional expense controls and AI-powered expense compliance? Traditional controls often check fixed rules, such as whether a receipt is attached or whether an amount exceeds a threshold. AI-powered expense compliance can review receipt details in context, analyze patterns, flag manipulated or fake receipts, and help auditors focus on higher-risk expenses. Emburse Assurance, for example, is described as reviewing full receipt images for context, authenticity, and accuracy.